65+

2022

We are a client-focused, results-driven partner committed to guiding you on your wealth-building journey.

BRB Capital is a global wealth management firm dedicated to helping individuals, corporations, and institutions grow and preserve wealth through innovative fund management, corporate advisory, impact financing, and investment strategies. With a data-driven approach and deep financial expertise, we empower our clients to achieve sustainable growth and long-term financial success.

To provide innovative and accessible financial solutions that help our clients achieve their financial goals with confidence.

Empowering financial growth for everyone, everywhere.

Our Core Values Speak Well

Innovation

Commitment to continuous improvement and staying ahead of industry trends.

Integrity

Upholding transparency, honesty, and ethical practices in all operations.

Customer Satisfaction

Prioritizing client needs and exceeding their expectations.

Inclusivity

Making financial growth accessible to all, regardless of socioeconomic status.

Covering the Full Spectrum of Global Financial Services

SEC Registered Portfolio management

We help you achieve your vision and cultivate confidence and peace of mind across your financial journey.

Client Experiences That Speak for Themselves

“BRB Capital didn’t just fund my business, they believed in the vision and walked the journey with me. BRB provided startup capital and strategic guidance that shaped the success of the business from the early stages of planning to the foundational steps of launching. Their commitment, insight, and genuine partnership have been instrumental, and I’m deeply grateful for their role in turning my ideas into a thriving enterprise.”

“Securing debt financing from BRB Capital was a game-changer for our healthcare financing business. It strengthened our working capital, enabling us to meet rising demand and expand strategically within the healthcare space. The competitive financing rate helped us optimize costs while scaling effectively. BRB Capital’s professionalism, efficiency, and deep understanding of our industry made the entire process seamless. We look forward to growing together.”

“Before BRB Capital, Juban Realty was just another small business trying to find its footing. For over four years, we operated passionately but lacked the structure and resources needed to scale. That changed when BRB Capital came into the picture. They believed in our vision, invested in our growth, and helped us build the structure that transformed our business. Today, Juban Realty is not just another real estate agency in Nigeria; we are a trusted brand, delivering value with confidence and clarity. BRB Capital didn’t just fund us; they empowered us.”

“BRB Capital revolutionized property management by bringing PropShake into the digital era. By developing and launching the PropShake App, BRB Capital ensured that residents of the facilities we manage enjoy seamless, transparent, and responsive services from the comfort of their mobile phones. This investment in digital transformation was driven by strategic industry insight, professionalism, and a genuine commitment to creating long-term value. Their insight-driven approach and dedication to tailored financial and technological solutions make them a trusted partner in driving sustainable growth and redefining facility management.”

- Report

December 2025 Inflation Report

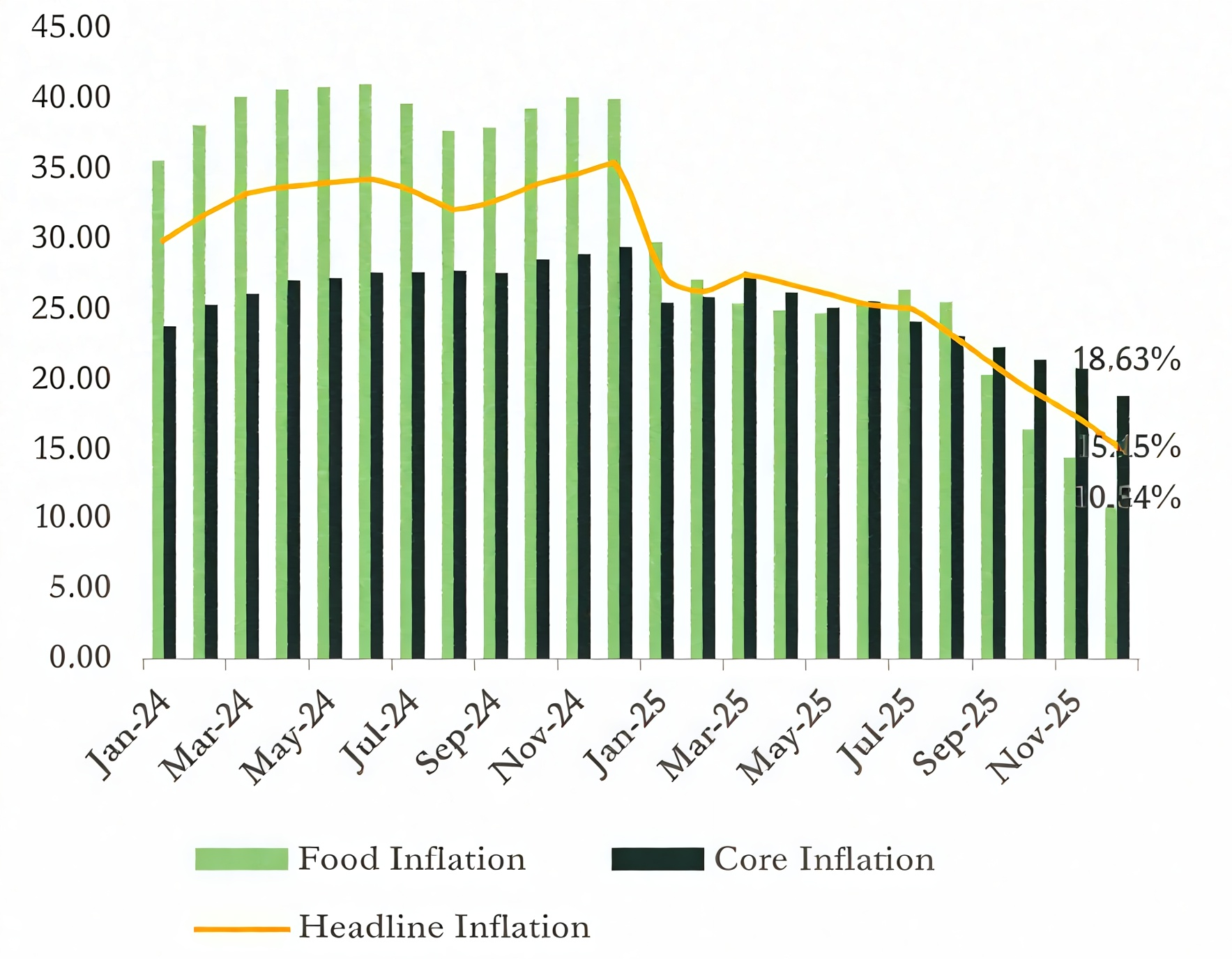

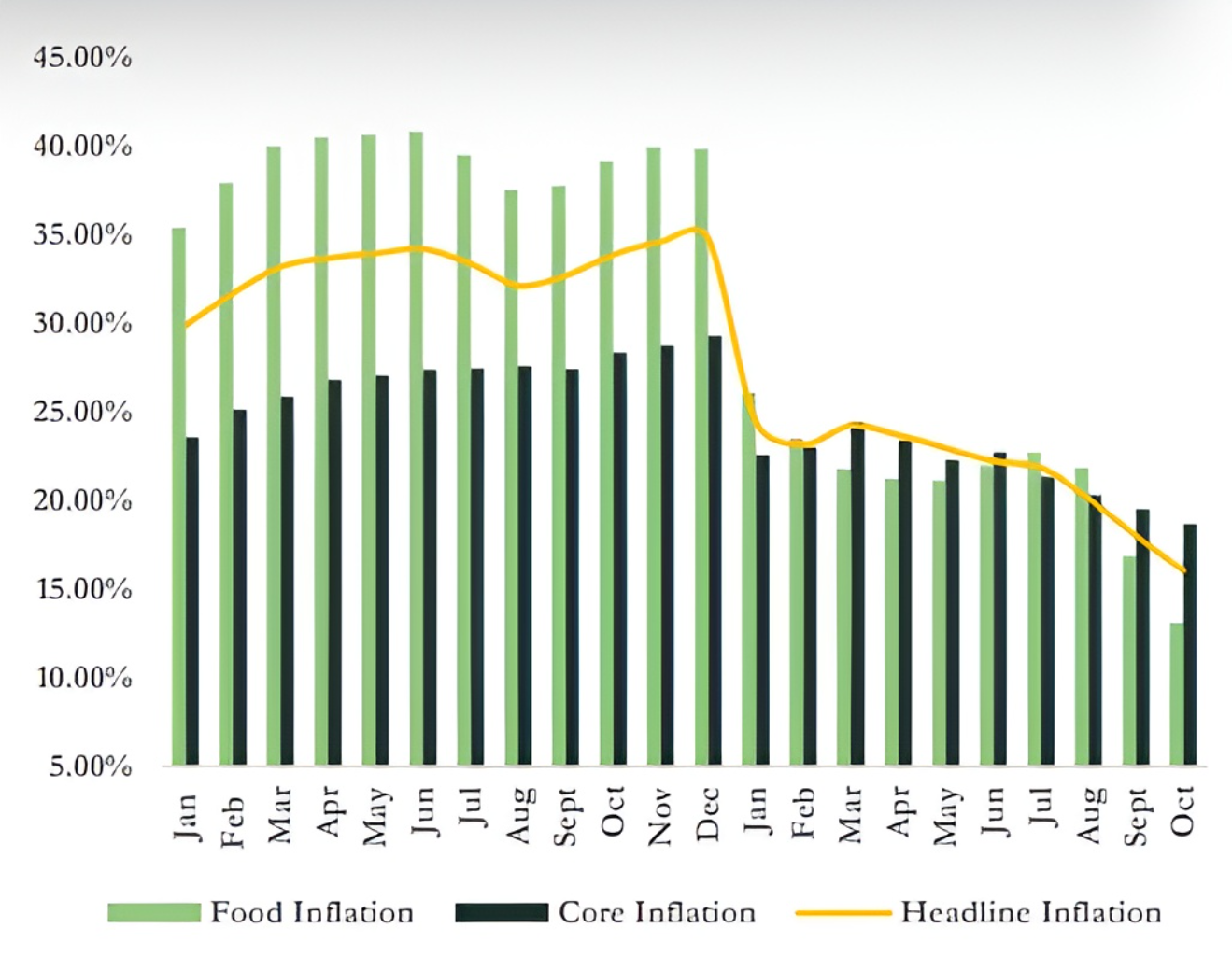

Inflation eased to 15.15% in December 2025 following an adjustment by the NBS.

Nigeria’s headline inflation moderated to 15.15% year-on year in December 2025, down from 17.33% in November, reflecting a methodological adjustment by the National Bureau of Statistics (NBS).

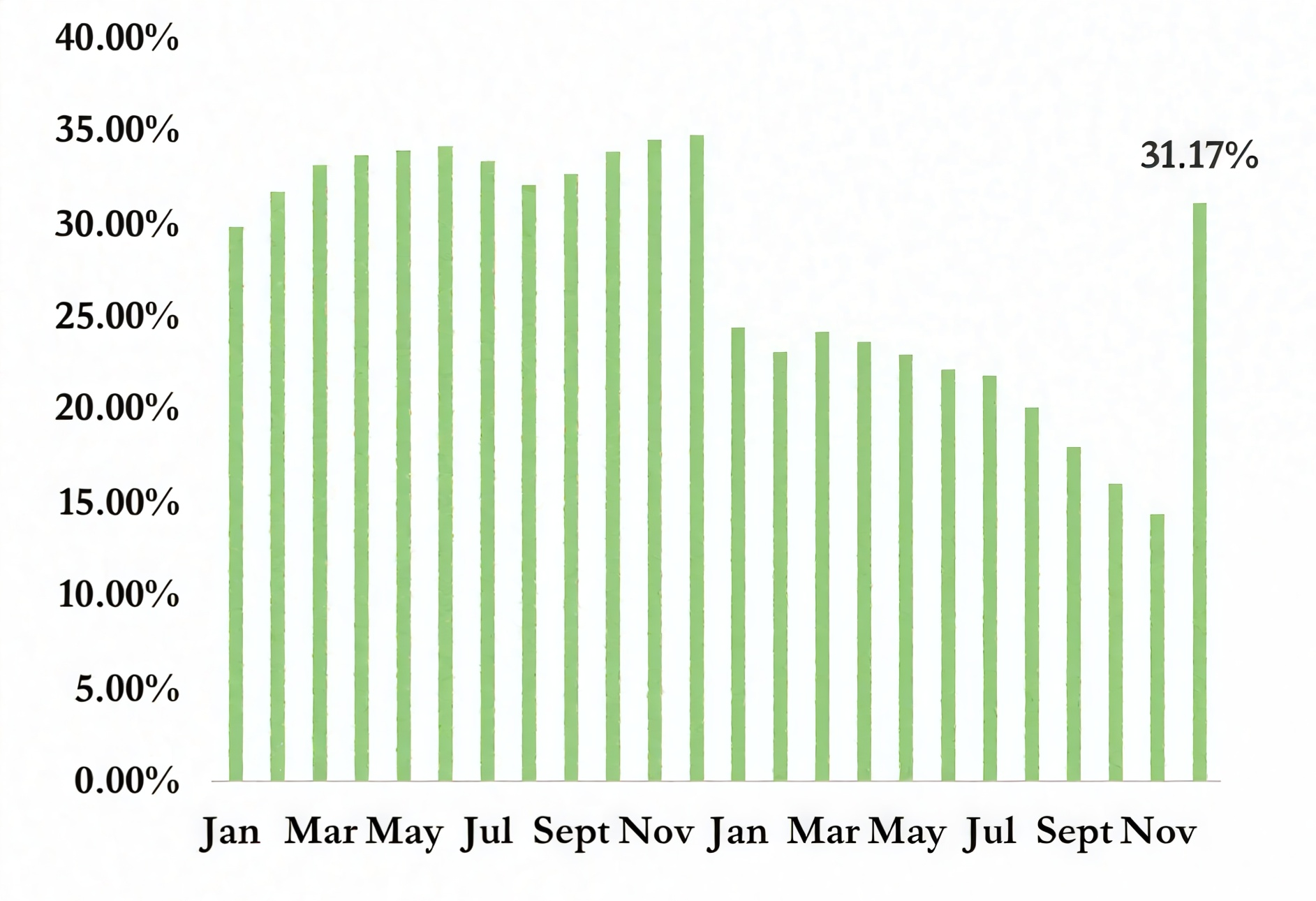

The decline follows the NBS’s adoption of a 12-month average CPI for 2024 as the reference period, replacing the previous single-month (December 2024) base. This change was implemented to eliminate an artificial inflation spike caused by base effects. Under the former methodology, headline inflation for December 2025 was projected to surge to about 31.2%, a distortion driven by the comparison base rather than a sharp acceleration in underlying price pressures. The revised approach, therefore, provides a more accurate representation of inflation dynamics, even as price levels remain elevated.

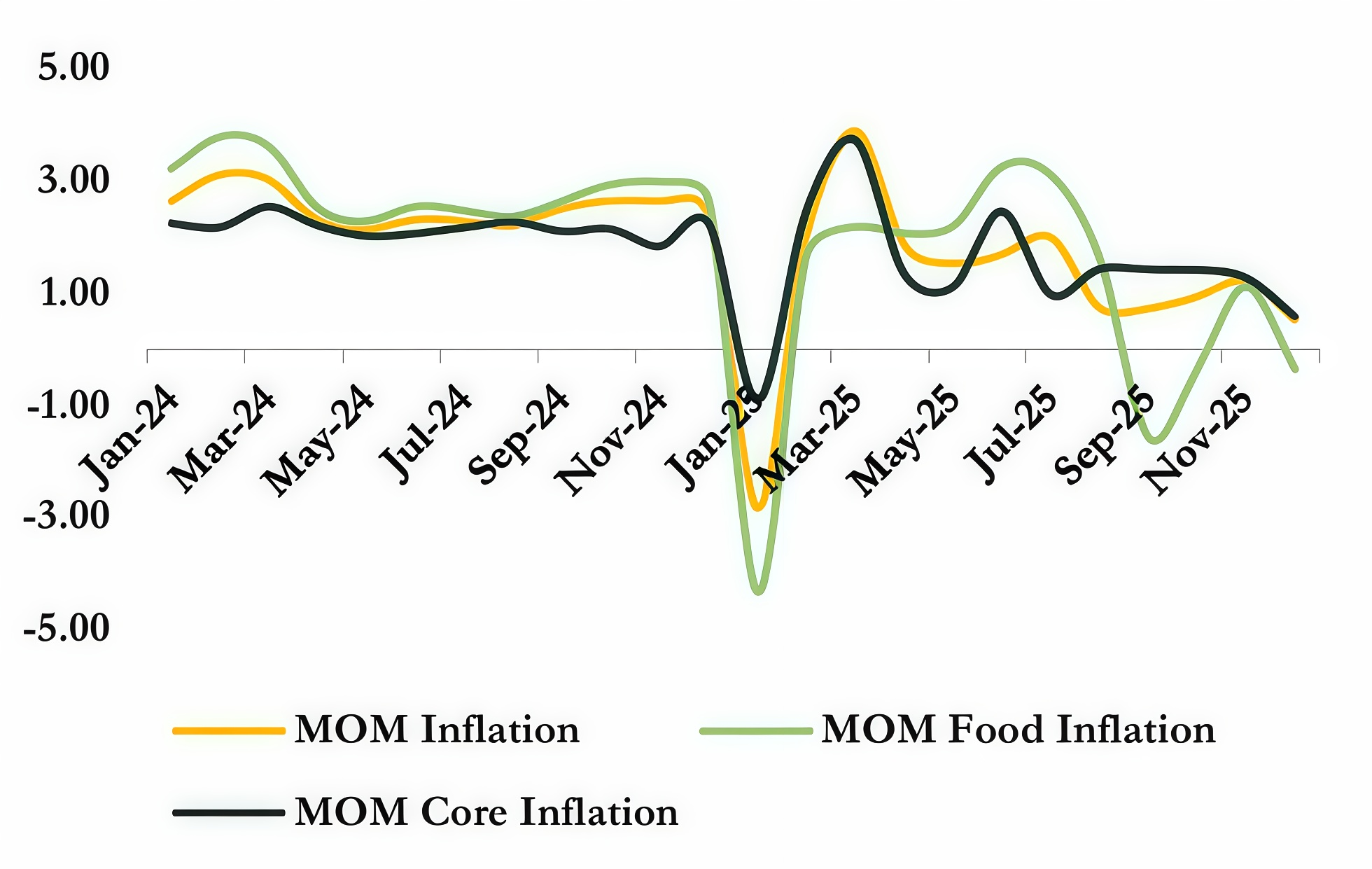

On a disaggregated basis, food inflation eased to 10.84% in December from 14.21% in November, while core inflation moderated to 18.63% from 20.59%, reflecting a broad based slowdown in price momentum following the methodological adjustment. On a month-on-month basis, headline inflation decelerated to 0.54%, down from 1.22% in the prior month. Food inflation turned negative at 0.36%, compared with 1.13% in November, suggesting easing short-term price pressures, while core inflation slowed to 0.58% from 1.28% previously.

OUTLOOK

We expect headline inflation to maintain a downward trajectory in 2026, supported by a relatively stable exchange rate, which should help moderate imported inflation pressures. Additionally, a weaker global oil market, driven by a projected supply surplus, could further ease global energy prices. However, this presents a double-edged risk: while lower energy prices may reduce domestic fuel costs and ease transportation and logistics expenses, weaker oil prices could also dampen export earnings and exert pressure on the naira, potentially offsetting gains through higher import costs.

On balance, the anticipated disinflation trend may create room for the Monetary Policy Committee to begin a gradual pivot away from its current hawkish stance, should macroeconomic conditions remain supportive.

Y-o-Y Inflation Trend New CPI Series

Y-o-Y Inflation Trend Old CPI Series

M-O-M Inflation Trend New CPI Series

- Report

Nigeria Economic Review

2025 Economic Review

Economic Growth Performance

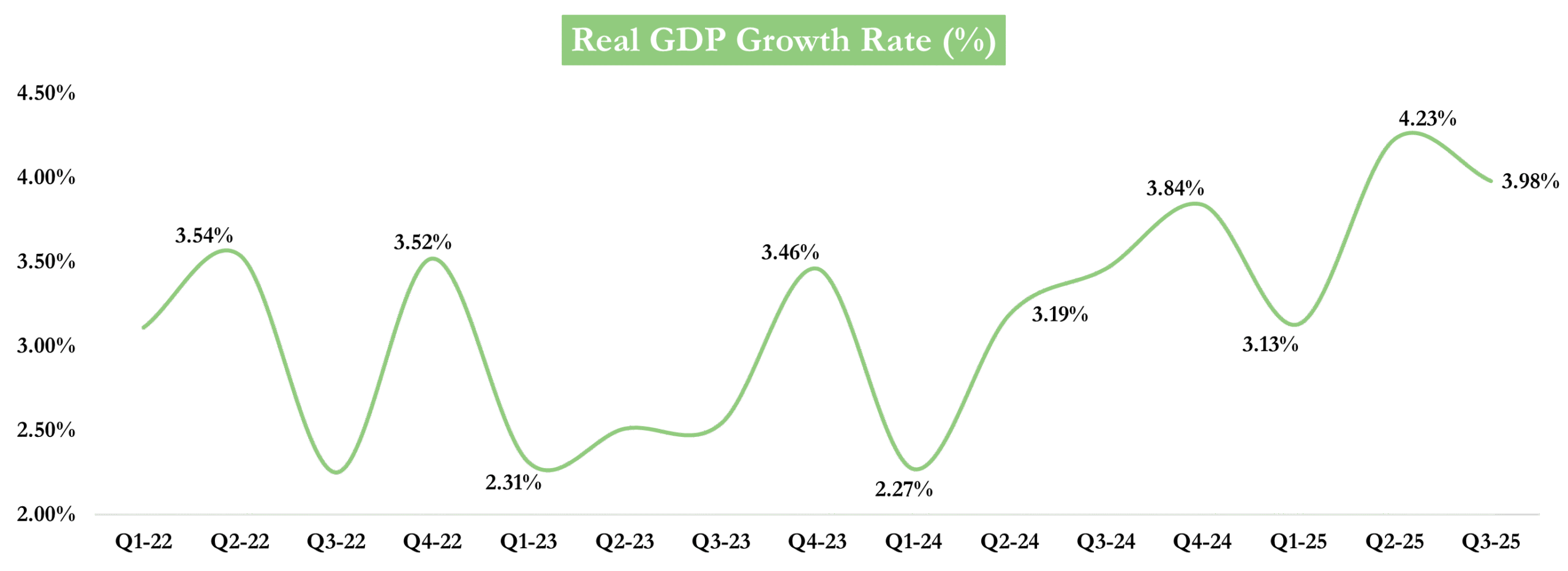

- Nigeria’s economy expanded by 3.98% y/y in Q3 2025, easing from 4.23% in Q2, its strongest growth since Q2 2021, but outperforming the 3.86% growth recorded in Q3 2024.

- The non-oil sector, which accounted for 96.6% of total output, grew by 3.91% vs Q2: 3.64%, supported by stronger activity in agriculture (3.79%), financial and insurance services (19.63%), trade (1.98%), construction (5.57%), and modest gains across ICT, real estate, and manufacturing.

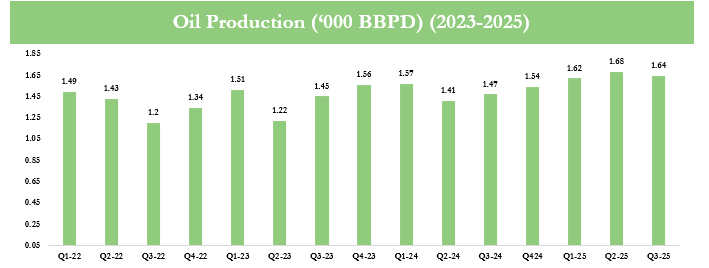

- In contrast, the oil sector grew by 5.84% y/y, a sharp slowdown from 20.46% in the previous quarter, reflecting weaker crude output. Oil production averaged 1.64 mbpd in Q3, slightly below Q2’s 1.68 mbpd but above the 1.47 mbpd recorded in Q3 2024.

Source: NBS, BRB Research

Inflation and Monetary Policy

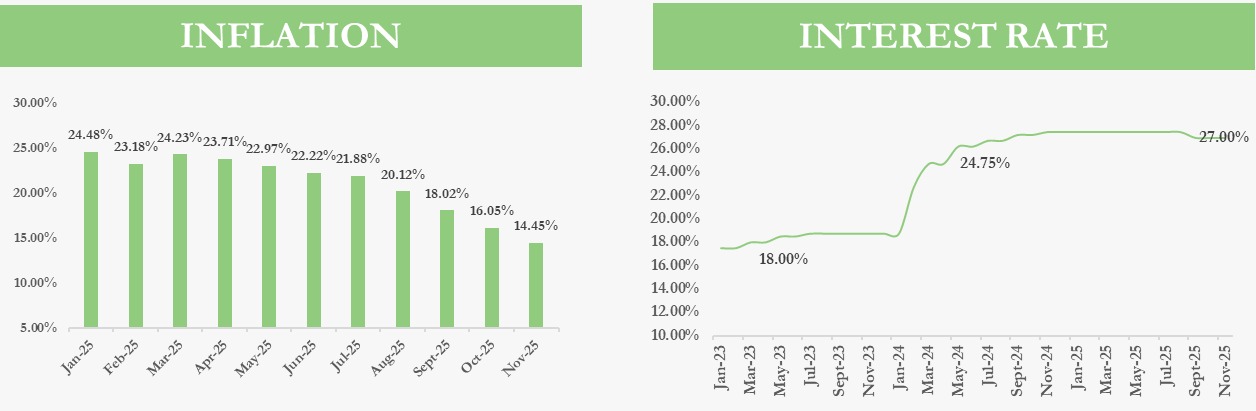

- Nigeria’s inflation environment has continued to improve, with headline inflation easing for the eighth consecutive month and settling at 14.45% from 16.05% year-on-year in November 2025. The deceleration has been driven largely by the rebasing effect, softer food price pressures, improved supply conditions, and a more stable foreign-exchange market. Core inflation remains elevated at 18.04% while Food inflation moderated to 11.08%, reflecting a gradual easing in underlying price pressures.

- Against this backdrop, the Central Bank of Nigeria maintained the MPR at 27% in November 2025, following a 50-bps reduction in September, as it sought to consolidate recent progress on disinflation. Although headline inflation continued to moderate, the MPC noted that underlying price pressures remain elevated, warranting a cautious pause. The adjustment of the policy corridor to +50/-450 bps from +250/-250 bps signals a subtly more accommodative liquidity framework. The stance shows a gradual shift from aggressive tightening toward a more balanced macro-stabilization

Source: NBS, BRB Research Source: Investing.com, BRB Research

Exchange Rate and Foreign Reserves

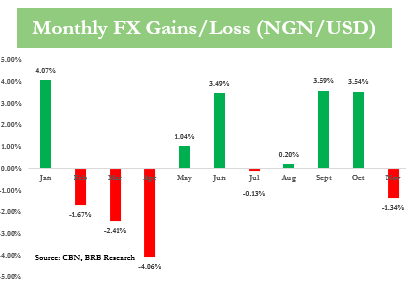

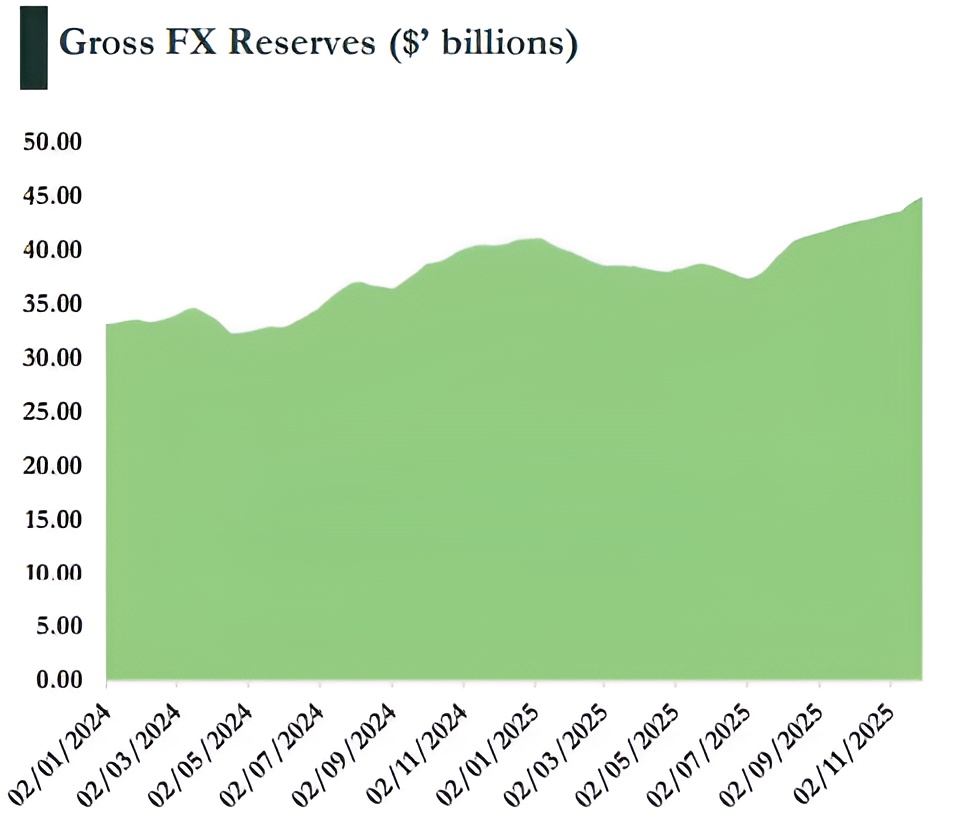

- Nigeria’s foreign exchange market stabilized in 2025 following previous periods of sharp depreciation, supported by CBN initiatives including the Electronic FX Matching System (EFEMS), transparent auction processes, and partial market liberalization. These measures enhanced liquidity and narrowed the gap between official and parallel market rates, with the naira strengthening to ₦1,446 per US dollar by November 2025 from ₦1,535 per US dollar at the end of 2024.

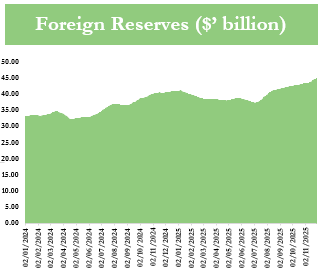

- Foreign reserves rose from USD 40.2 billion at the end of 2024 to USD 44.67 billion by November 2025, reflecting strengthened external sector conditions. The recent Eurobond issuance of $2.35 billion provided a significant boost to reserve buffers, complementing gains from improved oil production, firmer export receipts, steady remittance inflows, and renewed foreign portfolio investment.

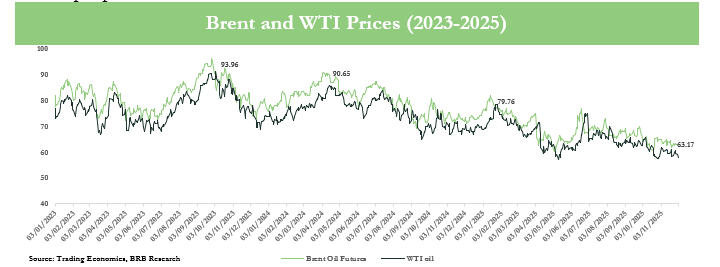

Oil Market

- The 2025 oil market began the year in relative balance, with temporary supply disruptions from seasonal factors and unplanned non-OPEC+ outages offset by robust structural supply. Demand growth remained moderate amid macroeconomic uncertainty, resulting in stable prices with limited volatility.

- In Q2, OPEC+ began rolling back voluntary production cuts while output from the U.S. and Brazil remained strong, leading to rising supply that outpaced demand and triggered bearish sentiment. By Q3, oversupply became the defining feature, as global production exceeded demand, inventories accumulated, and analysts revised downward full-year price expectations.

- The year closed with the supply glut persisting into Q4; inventories remained elevated, and prices stabilized below mid-year peaks following OPEC+ guidance on potential early-2026 output pauses.

Oil Production

- In Q3 2025, Nigeria’s average daily oil production stood at 1.64 million barrels, up 0.17 mbpd from Q3 2024 but slightly below Q2 2025’s 1.68 mbpd. The sector’s gradual recovery in 2025 was supported by improved security, enhanced pipeline integrity, and more coordinated upstream operations. Production averaged 1.66 mbpd in H1, peaked at 1.68 mbpd in Q2, the highest since 2020, and moderated slightly in Q3, reflecting ongoing operational adjustments and maintenance activities.

- The rebound helped reinforce external balances and foreign-exchange supply, but output volatility remained a feature of the sector’s performance. Despite the improvement, production levels fell short of the government’s 2025 target of 2.06 million barrels per day, reflecting ongoing structural challenges. Crude theft, infrastructure constraints, and intermittent operational disruptions continued to weigh on capacity utilization, limiting the pace of recovery.

Source: NBS, BRB Research

Economic Outlook for year 2026

2026 Outlook

- Nigeria’s economy is expected to expand over the near term, with the IMF projecting GDP growth of 3.9% in 2025 and 4.2% in 2026, supported by stable oil inflows, improving oil production levels, and greater policy consistency.

- Headline inflation is expected to continue its moderating trend in 2026, easing toward 11.56% by year-end, supported by a stable exchange rate, cautious monetary policy, and weaker energy prices. This disinflationary environment is likely to provide the Central Bank of Nigeria with scope to maintain a neutral to mildly accommodative monetary policy stance. We anticipate a potential recalibration of the MPR, with a projected easing of around 200 basis points by mid-2026, contingent on inflation remaining firmly anchored and underlying price pressures remaining subdued.

- Several risks could reverse the projected downward trend in inflation in 2026. Pressure on the exchange rate may increase the cost of imported goods, while elevated government spending ahead of elections could inject additional liquidity, boosting prices. Structural challenges, including insecurity in key food-producing regions, may constrain supply and exert upward pressure on food prices. External shocks, such as volatility in global oil markets, also represent a potential upside risk to inflation during the year.

- Despite these challenges, higher foreign reserve buffers and reforms in the foreign-exchange market, including enhanced transparency and more efficient EFEMS operations, should help limit exchange-rate volatility and strengthen overall broader macroeconomic stability. These developments, alongside easing inflation and relatively stable macro fundamentals, are likely to support investor sentiment and attract modest portfolio inflows over the course of the year.

- The macroeconomic environment nonetheless remains sensitive to external and domestic shocks. Oil-price volatility continues to pose the most significant risk to fiscal stability and FX supply, while uncertainty around the revised Capital Gains Tax framework and lingering security concerns may temper investor appetite in the near term. Even so, the broader environment suggests cautiously improving conditions for Nigeria’s asset management and investment industry in 2026.

- Global oil market dynamics will be pivotal for Nigeria in 2026, with a structural supply surplus expected to persist due to strong non-OPEC+ production from the U.S. and Brazil and a measured supply approach from OPEC+. Demand growth will remain concentrated in non-OECD Asia, while elevated inventories are likely to keep Brent crude in the mid-to-low $50s per barrel. A potential peace deal between Russia and Ukraine could further soften prices if sanctions on Russian oil are eased, adding additional barrels to the market. Although geopolitical disruptions could still trigger short-term volatility, sustained low prices may eventually dampen non-OPEC+ investment.

Equities Market Review

Nigeria Equities Market Performance 2025

The Nigerian equity market delivered a powerful yet volatile performance in 2025, emerging as one of the strongest markets globally. For most of the year, sentiment was supported by market-friendly reforms, resilient corporate earnings, improved foreign-exchange conditions and strong domestic liquidity.

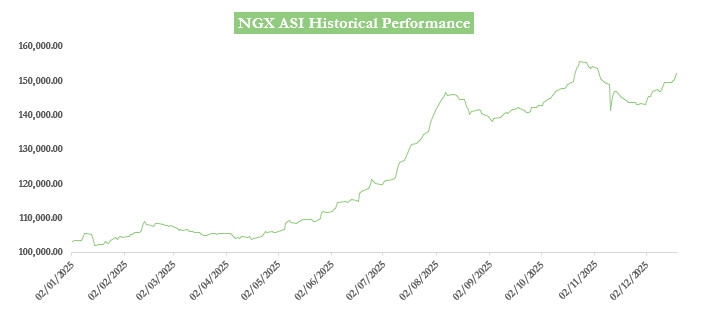

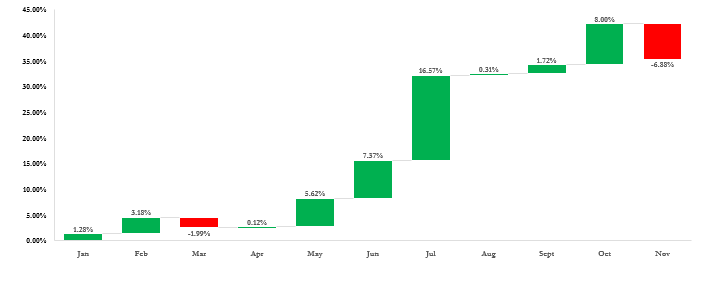

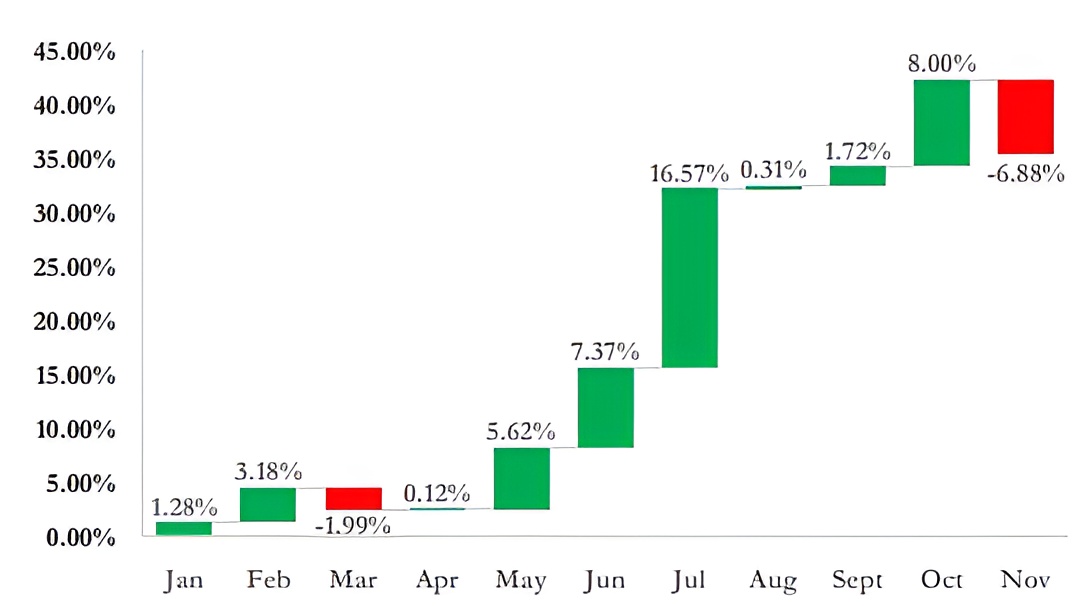

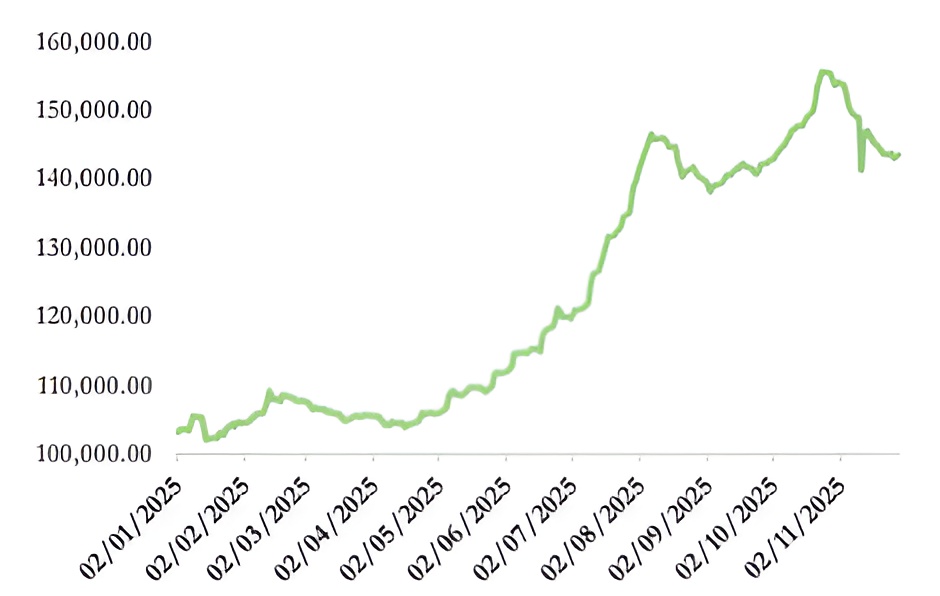

Market capitalization rose from ₦62.76 trillion at end-2024 to ₦91.29 trillion by late November, reflecting a 45.45% increase in investor wealth. Gains strengthened through the third quarter, with the ASI up 16.57% by mid-year and nearly 50% by October. The NGX All-Share Index (ASI) also advanced significantly, climbing from 102,926.40 points to over 150,000 points in October before moderating to 143,520.52 in November.

Investor participation was robust, driven by both domestic and foreign flows. Total transactions for the first eight months of the year rose by 99% to ₦6.92 trillion. Foreign portfolio inflows increased by 122% to ₦1.45 trillion, aided by improved FX liquidity and clearer exit conditions, whereas domestic investors contributed over ₦5.46 trillion, reinforcing their leadership in market activity. These flows were complemented by the performance of several high-growth stocks, with tickers like BetaGlass, MTN, Ellah Lakes, WEMA Bank, NCR, MBENEFIT, UACN, and ASO Savings delivering returns ranging between 100% and more than 500%, reflecting strong liquidity and high conviction in select counters.

NGX ASI Monthly Returns

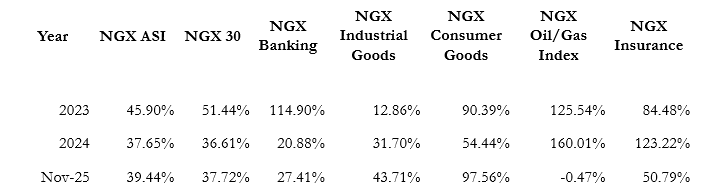

Sector performance highlighted the breadth of the rally. Consumer goods companies led with over 100% year-to-date gains by October, supported by strong local production and pricing resilience amid FX constraints. The Insurance Index rose sharply on recapitalization expectations, while the Banking Index, though third in returns, remained the most actively traded, reflecting strong institutional interest. Industrial goods stocks also saw significant demand, whereas the Oil & Gas Index lagged for most of the year due to sector-specific challenges.

NGX Sectoral Performance (2023-2025)

However, the positive momentum was interrupted in November by the sharpest correction of the year. Market capitalization fell by about ₦6.54 trillion following uncertainty over the proposed changes to the Capital Gains Tax framework. The shift from a flat 10% rate to a progressive structure of up to 30% triggered aggressive profit-taking and capital repatriation by foreign investors. Combined with geopolitical concerns, the policy announcement dampened sentiment and illustrated how quickly fiscal decisions can offset months of progress driven by monetary reforms and FX stability.

2026 Outlook

Outlook

Building on a robust 2025, Nigeria’s equities market is poised for a strong 2026 performance, with potential total returns exceeding 30%, supported by ongoing reforms, macroeconomic stability, and stronger corporate earnings. Key growth drivers include continued sectoral diversification, with consumer goods, industrials, and financials expected to anchor performance, alongside rising dividends that enhance total shareholder returns.

Market sentiment will be increasingly shaped by company-specific fundamentals, with investors focusing on earnings quality, balance sheet strength, and cash-flow resilience. The anticipated listing of NNPC Limited and Dangote Refinery next year could serve as a major liquidity and valuation catalyst, attracting both domestic and foreign capital.

Further support is expected from positive macroeconomic factors, including easing inflation, stable interest rates, and an improved foreign-exchange environment, as well as regulatory clarity that strengthens investor confidence. Active portfolio management, diversification across high-quality sectors, and close monitoring of earnings, FX developments, and policy changes will remain essential to navigate potential volatility and capture upside opportunities.

- Report

November 2025 Inflation Report

Inflation eased to 14.45% in November

Nigeria’s headline inflation rate eased to 14.45% year-on year in November 2025, down from 16.05% in October, marking the eighth consecutive month of disinflation and coming in below the Federal Government’s 2025 inflation target of 15.75%. The moderation was driven by a slowdown in both major components of inflation. Food inflation declined to 11.08% from 13.12%, while core inflation eased to 18.04% from 18.69%, reflecting softer price pressures across key non-food categories.

However, price pressures persisted on a month-on-month basis, with headline inflation rising to 1.22%, compared with 0.93% in October, indicating continued increases in price levels. The acceleration was largely food-driven, as food inflation rebounded to 1.13% from -0.37%, reversing the disinflation observed in the previous two months. This reflects renewed pressure from seasonal demand ahead of the festive period, alongside security-related disruptions in key food-producing regions that have constrained harvest activities.

In contrast, core inflation moderated to 1.28% from 1.42%, supported by slower price increases in financial services (0.18% vs 1.71%), education (0.02% vs 0.78%), and information and communication (0.12% vs 0.54%).

OUTLOOK

Looking ahead to November, we expect headline inflation to tick up in December 2025, driven by festive-related demand pressures and food supply constraints, with the increase amplified by base effects following the CPI rebasing.

Beyond this temporary rise, we anticipate the disinflation trend to resume from early 2026, potentially creating room for the Monetary Policy Committee to begin a gradual pivot

away from its current hawkish stance.

Y-o-Y Inflation Trend

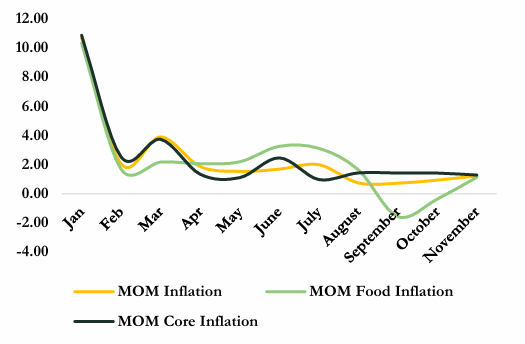

M-O-M Inflation Trend

- Insights

Monthly Market Brief (November 2025)

MACROS

In November 2025, the Central Bank of Nigeria (CBN) maintained a restrictive monetary policy stance, signaling a measured approach toward sustaining price stability and anchoring market expectations. At the 303rd Monetary Policy Committee meeting, the CBN held the Monetary Policy Rate at 27.0% and retained the Cash Reserve Requirement for deposit money banks at 45%, reflecting its commitment to liquidity sterilization and broader disinflationary objectives. The Standing Facility corridor was adjusted to +50/-450 basis points, a technical refinement designed to improve short-term liquidity management and tighten the transmission of policy signals to the money market.

The retention of the MPR followed the first-rate adjustment since September, demonstrating the MPC’s preference for caution. Policymakers emphasized that the cumulative effects of previous tightening cycles are still unfolding, and premature easing could undermine gains in inflation control and destabilize the foreign exchange market by weakening the yield differential that attracts portfolio inflows. This approach reflects the dual mandate of controlling inflation while preserving external sector stability.

October CPI data indicated continued disinflation, with headline inflation moderating to 16.05% year-on-year and month-on-month price growth slowing to 0.90%. However, underlying structural pressures persist. Core inflation, which excludes volatile food and energy components, remained elevated at 18.70%, driven by sustained cost pressures in housing, utilities, and transportation. Food inflation, at 13.12%, reflects the vulnerability of the agricultural sector to security challenges, including banditry and logistics disruptions, which continue to exert upward pressure on prices despite monetary tightening.

Inflation Trajectory

In November 2025, the Nigerian foreign exchange market continued to consolidate stability, reflecting the effectiveness of the CBN’s unification and market-driven reforms. The Naira traded steadily around the mid-₦1,440/US$ range, posting a monthly depreciation of -1.34%. The elimination of the chronic arbitrage

premium underscores the success of structural reforms, enhancing investor confidence and supporting efficient market functioning.

The currency’s resilience was underpinned by a combination of restrictive monetary policy, robust foreign portfolio inflows, and structural measures to expand non-oil FX supply, including the NRBVN platform to facilitate diaspora remittances. High interest rates remain a key tool in attracting capital, though they create a structural reliance on foreign inflows for stability.

Nigeria’s external sector strengthened markedly, with Gross External Reserves rising to US$46.7 billion by mid-November, equivalent to 10.3 months of import cover. The successful US$2.35 billion Eurobond issuance contributed to reserve accumulation, reinforcing Nigeria’s capacity to absorb external shocks and maintain macroeconomic stability

EQUITIES

The Nigerian equity market in November 2025 experienced a sharp correction as fiscal policy uncertainty and restrictive monetary conditions combined to trigger widespread profit-taking and capital flight. The NGX All-Share Index dropped from 154,126.46 points at the end of October to 143,520.53 points by 28 November, reflecting a month-to-date decline of 6.88%. Similarly, market capitalization shrank by ₦6.54 trillion, declining from ₦97.83 trillion to ₦91.29 trillion. Despite the pullback, the year-to-date gain remained positive at 39.44%, still lower than the 49.74% recorded at the end of the previous month, reflecting the strong rally seen earlier in 2025.

The market downturn was primarily driven by profit-taking activities and the government’s announcement of an increase in the capital gains tax for foreign investors from 10% to 30% on non-reinvested equity sales, effective January 2026, which prompted foreign portfolio investors to realize gains under the existing lower tax regime. Concurrently, the Central Bank of Nigeria maintained a rigid monetary tightening stance, keeping the Monetary Policy Rate at 27.0%, further discouraging equity speculation and sustaining pressure on valuation multiples.

NGX ASI Monthly Returns

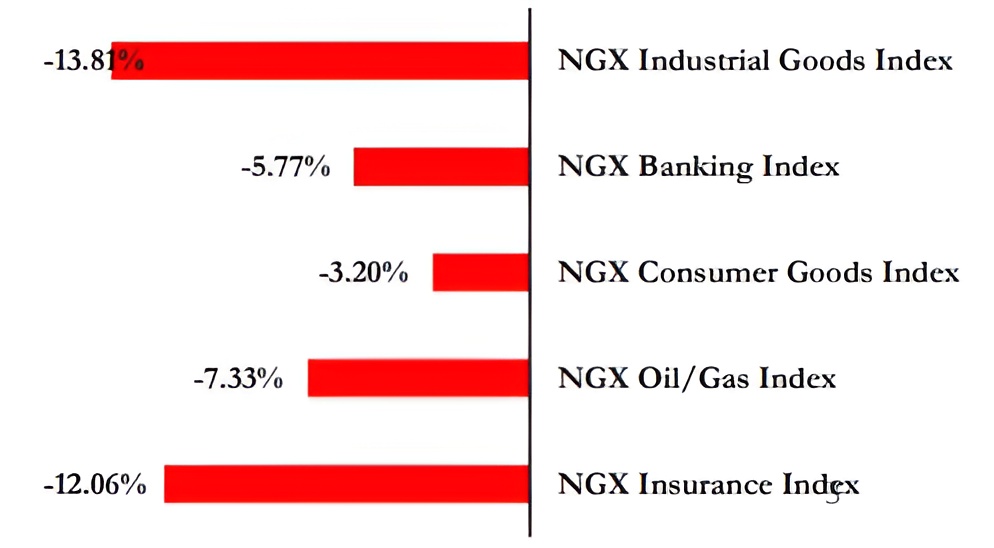

Sectoral performance across the Nigerian Exchange in November 2025 reflected a broad-based market retreat driven by sharp foreign portfolio outflows and sustained monetary tightening. The Industrial Goods Index recorded the steepest decline at –13.81% (vs. +17.50% in October), as major cement names, DANGCEM (–19.00%), BUACEM (–11.11%), and WAPCO (–4.29%), faced heavy selloffs following the announcement of the 30% capital gains tax on nonreinvested foreign equity sales. Earlier valuation gains, boosted by FX-driven earnings expansion, unwound quickly under higher discount-rate conditions.

The Banking Index fell –5.77% (vs. –3.15%), pressured by broad profit-taking and portfolio repositioning. Tier-1 names such as ACCESSCORP (–14.11%), GTCO (–12.28%), UBA (–8.99%), Zenith (–4.76%), and WEMA (–10.51%) declined as elevated liquidity constraints, particularly the 45% CRR, kept funding conditions tight. Although strong earnings fundamentals encouraged intermittent bargain hunting, they were insufficient to offset overall downside momentum.

NGX ASI Historical Performance

Consumer Goods slipped –3.20% (vs. +4.85%), reflecting a relatively defensive pullback. Losses in Champion (–17.33%), Nestle (–7.05%), Cadbury (–7.43%), and DangSugar (–7.60%) weighed on the index, though domestic-focused midcaps such as Unilever showed resilience and helped drive a mild late- month rebound, including a 0.57% uptick on November 28.

The Oil & Gas Index contracted –7.33% (vs. +15.45%), driven by profit-taking in ARADEL (–11.76%) and OANDO (–19.15%) amid weaker sentiment toward energy names due to global crude uncertainty and domestic macro risks. Insurance posted one of the sharpest declines at –12.06% (vs.+3.37%), as risk aversion triggered broad sell pressure across small- and mid-cap counters. AIICO (-15.35%), NEM (14.74%), and MBENEFIT (- 13.95%) were the major drivers of the loss.

Overall, November’s performance was dominated by aggressive divestment linked to fiscal policy signals, particularly the CGT announcement, overshadowing sectorspecific fundamentals. While select rebounds emerged toward the month-end, sectoral dynamics remained shaped by tight monetary conditions, fragile investor sentiment, and a pronounced rotation away from high-beta Nigerian equities.

NGX Sectoral Returns in November

In line with this broad weakness, several blue-chip counters were also among the worst-performing stocks for the month, reflecting the heavy divestment pressure triggered by the CGT announcement.

High-beta, foreign-held names such as DANGCEM (–19.00%), ACCESSCORP (–14.11%), GTCO (–12.28%), UBA (–8.99%), Zenith Bank (–4.76%), and NESTLE (–7.05%) saw sharp declines as investors exited large-cap positions to rebalance risk.

Nonetheless, a few tickers bucked the trend, with NCR (+241.56%), Ikeja Hotel (+60.90%), Eunisell (+37.29%), and UACN (+18.65%) emerging as notable outperformers, largely driven by companyspecific developments and their previously low-price levels, rather than the overall market trend.

Outlook

Market sentiment entering December is expected to remain cautious, despite the federal government’s clarification of the 30% CGT, which introduced key provisions such as grandfathering for pre-2026 gains, exemptions for retail portfolios below ₦150 million, and reinvestment relief. This will ease investor anxiety and create room for cautious re-entry, though liquidity remains tight and macroeconomic conditions continue to limit risk-taking. The rollout of the CBN’s new fixed-income trading and settlement framework will also be closely watched, as any operational disruptions could affect secondary-market liquidity and influence portfolio positioning.

Despite these headwinds, December may still benefit from seasonal drivers such as dividend positioning, year-end rebalancing, and selective bargain-hunting following November’s valuation reset. However, sustained recovery will depend on consistent policy execution, improved communication, and early signs of monetary easing. Until these conditions improve, overall market posture is likely to remain defensive, with investors prioritizing stability while gradually rebuilding exposure ahead of the 2026 trading year.

FIXED INCOME

Domestic Money Market and System Liquidity

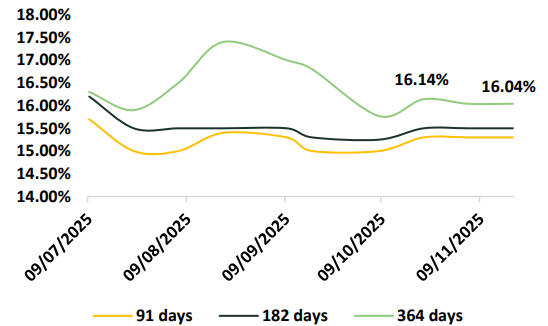

The Nigerian Treasury Bills (NTB) market in November 2025 recorded strong, yield-sensitive demand as investors sought safety amid heightened equity-market volatility and tight monetary conditions. Elevated system liquidity and attractive sovereign yields supported aggressive bidding across all tenors, particularly the 364-day maturity, as investors aimed to lock in double-digit rates ahead of potential monetary policy adjustments in early 2026. Throughout the month, the primary market remained a key destination for domestic institutional funds, reflecting a strategic reallocation toward risk-free assets.

The early-November auction on November 5 set the demand tone for the month, with stop rates clearing at 15.30% (91-day), 15.50% (182-day), and 16.04% (364-day). Despite relatively modest issuance sizes, subscription levels, especially the ₦1.14 trillion demand for the 364-day bill, far exceeded offer amounts, underscoring the strength of investor appetite for longer tenor bills. The tight bidding bands reflected disciplined pricing, driven by expectations that yields were near their cyclical peak and could moderate in subsequent months. These conditions led investors to prioritize locking in term yields while seeking tactical duration exposure.

A major inflection in the yield environment emerged in mid-to-late November following the Monetary Policy Committee’s decision to maintain the MPR at 27.0%, which helped stabilize rate expectations. This policy continuity enabled the CBN to engineer a substantial downward adjustment in stop rates during the November 19 auction. The 364-day rate dropped sharply to 16.04%, a notable decline from the 20%+ levels recorded in mid-month auctions, while subscription still reached ₦1.03 trillion (2.3x oversubscription). The successful rate compression demonstrated the CBN’s capacity to exert decisive

control over front-end yields, exploiting deep domestic liquidity to reduce government borrowing costs while maintaining strong participation.

Eurobonds and Global Confidence

Nigeria’s engagement with the international capital markets in November 2025 was defined by a strong primary issuance outcome juxtaposed against renewed secondary-market volatility. The country’s US$2.35 billion Eurobond deal, issued across 10-year and 20-year tranches, attracted exceptionally strong investor interest, reflecting ample global liquidity and sustained appetite for high-yielding emerging-market sovereign debt. However, the supportive issuance backdrop contrasted with a wider recalibration of risk premiums in secondary trading as global conditions became less favourable toward emerging-market assets.

The primary issuance on 5 November 2025 saw Nigeria successfully price US$1.25 billion of 10-year notes at 8.625% and US$1.10 billion of 20-year notes at 9.125%. Demand was exceptionally robust, with the order book reportedly surpassing US$13 billion, translating to roughly 12x oversubscription, one of the largest ever recorded for a Nigerian sovereign sale. While the strong subscription secured the government’s target capital for deficit financing, the elevated pricing levels underscored that investor enthusiasm was overwhelmingly yield-driven. Despite the large order book, markets required materially high coupons to compensate for Nigeria’s fiscal vulnerabilities, reserve adequacy concerns, and broader macro risk environment.

In contrast to the upbeat primary-market experience, Nigeria’s existing Eurobonds posted mixed performance throughout November. Secondary market yields widened by 32 basis points on average, closing at 7.97%, reflecting renewed selling pressure across the curve. This repricing indicated that the market remained sensitive to shifts in global risk appetite, with investors demanding additional term premium to hold Nigerian debt despite the successful primary issuance. The divergence between primarymarket strength and secondary-market weakness further highlights the distinction between issuance-driven liquidity dynamics and underlying credit-risk perceptions.

Two key external factors shaped this upward yield drift. First, a strengthening of the U.S. dollar contributed to modest shifts away from emerging-market hard-currency bonds, raising funding costs for sovereigns like Nigeria. Geopolitical tensions between the United States and the Nigerian government also pushed yields higher. After the U.S. issued strong political warnings about Nigeria’s internal security situation, investors became more cautious. The resulting increase in yields illustrates Nigeria’s structural sensitivity to non-economic shocks and underscores the risks inherent in relying heavily on Eurobond financing. As global conditions remain fluid, Nigeria’s external debt trajectory will depend increasingly on stabilizing domestic macro fundamentals and rebuilding investor confidence in its long-term credit outlook.

FIXED INCOME

The Federal Government of Nigeria (FGN) conducted bond auctions on November 24, 2025, offering ₦230 billion each of the 17.945% FGN AUG 2030 (5-Year) and 17.95% FGN JUN 2032 (7-Year) bonds. Subscription levels highlighted stronger investor interest in the medium-term tenor: the 7-Year bond recorded a subscription of ₦509.392 billion, compared to ₦147.869 billion for the 5-Year bond. Successful allotments amounted to ₦448.722 billion and ₦134.799 billion, respectively, reflecting moderate oversubscription for both instruments.

Yields were set at 15.900% for the 5-Year bond and 16.000% for the 7-Year bond, below the initial coupon rates, signaling effective yield management by the Debt Management Office (DMO). The noncompetitive allotment of ₦6.0 billion for the 7-Year bond also underscores continued demand from smaller investors and domestic institutions.

The auction outcomes suggest stabilizing borrowing costs for the federal government, with minimal upward pressure on yields. Coupled with recent trends in T-Bills and short-term securities, the results indicate a coordinated approach to maintaining domestic debt market stability, reflecting investor confidence in Nigeria’s debt instruments amid prevailing macroeconomic conditions.

OUTLOOK

The Nigerian fixed-income market is set for a gradual recalibration. With the CBN maintaining tight monetary conditions and ample liquidity, short-term NTB yields are expected to ease, providing investors with opportunities to secure attractive returns ahead of potential rate adjustments. Demand for longer-dated government bonds remains robust, supported by stable coupon payments and potential capital appreciation in a moderating yield environment.

Fiscal discipline and strategic debt management will be key. A shift toward lower-cost, long-dated instruments, including diaspora bonds, Sukuk, or green bonds, combined with efforts to diversify non-oil revenues, could enhance debt sustainability and bolster investor confidence. This outlook depends on continued macro stability, easing inflationary pressures, and contained external debt risks.

On the external front, while Eurobond issuances have drawn strong demand, global rate dynamics and geopolitical risks could pressure yields, underscoring the need for vigilance. Overall, highyield, long-term government debt is likely to remain a preferred allocation in the near to medium term, contingent on stable macro fundamentals and consistent policy execution.

- Report

Post MPC Meeting Report (November Meeting)

MPC RETAINS INTEREST RATE AMID DISINFLATIONARY TREND

The Monetary Policy Committee (MPC) of the Central Bank of Nigeria concluded its 303rd meeting on November 25, 2025, delivering a policy stance characterized by headline rate stability and technical tightening through adjustments to operational tools. While the benchmark rate was held constant, the recalibration of the asymmetric corridor signals a continued commitment to disinflation, FX stability, and prudent liquidity management.

Policy Decisions and Rationale

The MPC opted for continuity in its primary policy levers:

- MPR: Retained at 27.00%, reinforcing the CBN’s tight monetary posture.

- CRR: Maintained at 45% for DMBs, 16% for merchant banks, and 75% for non-TSA public sector deposits

- Liquidity Ratio: Held steady at 30%.

- Asymmetric corridor was adjusted to +50/-450bps from the previous +250/-250bps around the MPR

The most notable action was the adjustment of the asymmetric corridor to +50/-450 bps around the MPR, resulting in a 27.5% Standing Lending Facility (SLF) and a 22.5% Standing Deposit Facility (SDF). This shift away from the previously wider symmetric corridor effectively tightens the lower bound of system liquidity, discouraging excess reserves and strengthening monetary transmission. The Committee emphasized that maintaining this stance allows the lagged effects of earlier rate hikes to permeate the economy, given the ongoing disinflationary trend.

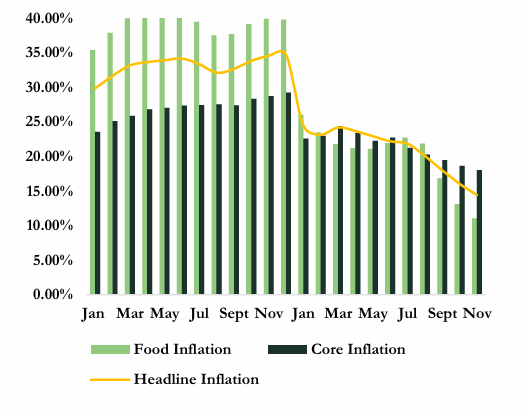

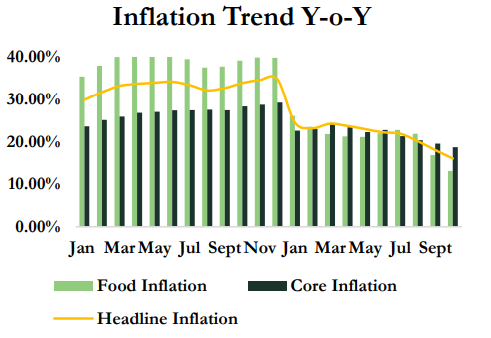

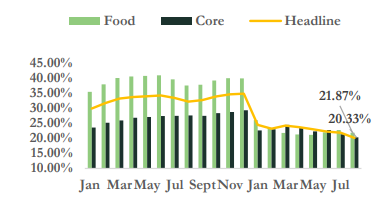

Inflation continued its steady downward trajectory in October 2025, marking the seventh consecutive month of disinflation. Headline inflation declined to 16.05% (y/y) from 18.02% in September, reflecting broad-based moderation across both food and core components.

Food inflation eased sharply to 13.12% from 16.87% in the previous month. This improvement was supported by improved domestic food supply associated with the seasonal harvest cycle, sustained exchange rate stability, and favourable base-year effects. Meanwhile, core inflation slowed to 18.69% (y/y) from 19.53%, driven largely by lower prices in furnishing and household maintenance categories.

Inflation Trend Y-o-Y

Despite these positive developments, the MPC emphasized that inflation remains elevated in double digits, underscoring the need for persistent policy vigilance to sustain and deepen the disinflation trend. The MPC noted that the broad-based deceleration across headline, food, and core measures reflects the combined effect of past tightening, exchange-rate stabilization, and improved domestic supply conditions. The Committee expects this disinflationary momentum to persist into the near term.

The MPC’s emphasis on persistently high core inflation, which remains above the headline rate, reinforces the view that underlying price pressures are structural rather than transitory. This validates the Committee’s cautious posture and signals that broad monetary easing will not commence until inflation expectations are firmly anchored and macroeconomic stability is consolidated.

The Global View

On the global front, the CBN assessed a cautiously improving environment. Global output is projected to strengthen on improved trade negotiations, accommodative policies in advanced economies, and easing geopolitical tensions. However, risks remain from potential protectionism, geoeconomic fragmentation, and renewed U.S.–China trade frictions. Global inflation is projected to continue moderating into 2026.

Domestically, the MPC highlighted the strong external sector position, supported by a surplus current account, continued reserve accretion, and Stable FX market conditions. These improvements, alongside collaborative fiscal–monetary reforms, supported recent upgrades to Nigeria’s sovereign rating and the country’s delisting from the FATF grey list, strengthening investor confidence.

Market Impact

The MPC’s decision to hold the MPR at 27% disrupted expectations for a sizeable rate cut, preventing the

significant yield compression previously anticipated across the money and bond markets. This outcome stabilizes fixed-income pricing by reducing immediate downside risk to asset values and provides clearer rate visibility after recent market volatility.

In the Treasury Bills and OMO segments, yields are expected to remain elevated. The latest auction results show the 364-day NTB marginal rate at 16.04%, broadly aligned with headline inflation at 16.05%. This ensures short-term instruments continue to deliver attractive real returns, supporting strong investor demand under the high-interest-rate environment.

From a portfolio positioning standpoint, the policy hold reinforces an Overweight bias toward short- to mid-tenor sovereign securities, where yields remain compelling and liquidity conditions tight. Demand for NTBs, OMOs, and 3–7-year FGN bonds is expected to stay robust, given banks’ need to manage liquidity under elevated CRR pressures and limited alternative outlets.

Equity market implications are mixed. A selective approach is warranted, emphasizing fundamentally strong, dividend-paying companies with sustainable pricing power. Large-cap banks are likely to maintain earnings resilience through elevated net interest margins, while firms with significant FX revenues stand to benefit from exchange-rate stability. Conversely, highly leveraged manufacturers and consumer-facing companies reliant on expensive domestic credit remain vulnerable under the prolonged tight monetary stance.

Outlook

The Committee projects that disinflation will continue in the near term, driven by the lagged effects of previous policy tightening, stable FX conditions, and improved domestic food supply associated with the seasonal harvest cycle. However, inflation remains elevated, and the MPC is expected to maintain a restrictive stance until a more durable decline in core and headline inflation is secured.

For financial markets, this suggests a continued environment of high yields, tight liquidity, and selective risk-taking. Fixed-income valuations will remain anchored by the elevated policy rate, while equity performance will diverge along sectoral and balance-sheet strengths.

The next MPC meeting is scheduled for February 23–24, 2026, where the trajectory of inflation, FX stability, and fiscal alignment will determine whether current tightening is sustained or provides room for cautious policy recalibration.

Hear Directly

From BRB Capital Experts

- Report

Post MPC Meeting Report

MPC LOWERS INTEREST RATE AMID DISINFLATIONARY TREND

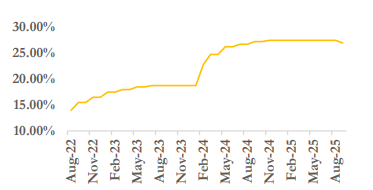

At the conclusion of the 302nd Monetary Policy Meeting (MPC) on 22nd and 23rd September 2025, the MPC voted to cut the Monetary Policy Rate (MPR) by 50 basis points from 27.50% to 27%, marking the first interest rate cut since September 2020.

Other key decisions include a reduction of the Cash Reserve Ratio (CRR) for Deposit Money Banks (DMB) by 500bps to 45.00%, while keeping the CRR for Merchant Banks at 16.00%. The MPC also retained the Liquidity Ratio at 30.00% and adjusted the Asymmetric Corridor to +250/-250bps around the MPR. Additionally, a 75.00% CRR on Non-TSA public sector deposits was introduced.

Interest Rate

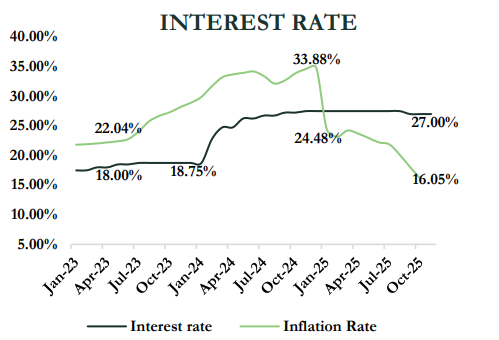

This reflects a shift from the hawkish stance of the MPC since its monetary policy tightening cycle in 2023, with the intention to curb inflation. The MPR was raised from 18.50% in 2023 to 27.50% in November 2024, which was maintained in 2025.

Nigeria’s headline inflation eased for the fifth consecutive month in August 2025 to 20.12%, largely driven by the rebasing effect, a reduction in food and core inflation components, and relative stability in the Naira.

Inflation Rate

The Global View

The CBN’s decision to lower the interest rate is in line with the global monetary authorities. The US Federal Reserve cut the federal funds rate by 25bps in September 2025, bringing it to 4.00%–4.25%. Conversely, the BoE and the ECB held rates steady at 4% and 2.15% respectively, following a monetary easing cycle since 2024.

Shifting gaze to Africa, Ghana implemented a 350bps rate cut to 21.5% in September. Similarly, the Central Bank of Kenya and the Central Bank of Egypt lowered their interest rates by 25bps and 200bps to 9.5% and 22%, respectively, while the South African Reserve Bank left its interest rate unchanged at 7%.

The CBN’s move to lower interest rates is backed by the continued disinflationary trend, resilient output growth, stable exchange rate, and robust external reserves. The MPC noted their satisfaction with macroeconomic stability as shown by improved inflation, stable Naira, stronger economic growth and robust FX reserves.

Impact Of Rate Cut

The CBN’s 50bps rate cut to 27%, reduction of banks’ CRR to 45% and the adjusted Asymmetric Corridor to +250/-250bps signal a shift toward stimulating growth after years of tight policy.

For banks, this provides improved liquidity, lower funding costs, and opportunities to expand credit to households and businesses (Corporate and SMEs). The move may also support asset quality as borrowers face reduced debt servicing costs, while easing could lift investor sentiment toward banking stocks and drive moderate margin improvements. The CBN’s imposition of a 75% CRR on non-TSA public deposits also drains liquidity, partly offsetting the benefits of the easing.

For the fixed income market, yields are likely to decline as liquidity improves and borrowing costs fall, lifting prices in the short term. This offers existing bondholders capital gains.

Overall, the policy creates a more enabling environment for lending, investment and growth in the economy. We expect a cautious easing stance from the CBN in the next meeting.

- Financing, Venture Capital

The Venture Capital Landscape: BRB’s Perspective

Accelerating Economic Development, the VC way

Venture capital (VC) has emerged as a catalyst in Nigeria’s journey toward sustainable economic growth and diversification. Traditionally reliant on oil and gas, the Nigerian economy is undergoing a paradigm shift toward innovation, entrepreneurship, and technology-driven solutions. VC is at the heart of this transformation, providing the critical financial resources, expertise, and strategic support that early-stage and high-growth startups require to thrive.

VC funding accelerates the development of sectors vital to Nigeria’s economic future, including financial technology (fintech), agriculture, clean energy, healthcare, and logistics. By backing entrepreneurs who address local challenges with scalable solutions, venture capital not only fosters the growth of individual businesses but also stimulates job creation, boosts productivity, and drives the adoption of new technologies across the broader economy.

By bridging the financing gap for startups and supporting Nigeria’s young and dynamic population, VC is catalysing a new generation of enterprises that are reshaping Africa’s economy. Its continued expansion is fundamental to unlocking Nigeria’s potential and achieving inclusive, technology-driven prosperity. Over the past decade, Nigeria has emerged as a pivotal hub for technology startups in Africa, driven by factors such as a burgeoning youth population, increasing internet penetration, and a growing appetite for digital solutions.

2024 VC Trends: Investment Climbs Globally, Contracts in Africa

According to the 2024 AVCA report, global venture capital investment reached US$313.6 bn, marking a 10% increase from the US$285.2 bn recorded in 2023. This figure accounts solely for VC deal volume and value, with deal values including Mezzanine and debt when the latter is part of a larger transaction that also involves equity. In contrast, Africa VC activity experienced a downturn in 2024, with US$2.6 bn invested across 427 deals, down from US$3.6 bn and 545 deals in 2023. This represents a 28% decline in value and a 22% drop in volume, highlighting a contraction in funding activity across the continent.

Despite this pullback, the 2024 figures suggest that Africa’s venture capital landscape may be approaching its peak. Notably, multi-region startups are shifting away from pan-African expansion strategies in favour of broader emerging market growth models. Leveraging later-stage capital, these startups are increasingly scaling into new geographies such as Southeast Asia, Latin America, and other developing regions, reflecting a strategic pivot toward global market diversification amid changing funding dynamics

The “Big Four” Dominate as FinTech Attracts the Lion’s Share of Funding

In 2024, West Africa maintained its lead in deal volume for the fourth consecutive year, driven primarily by Nigeria, which was the most active country by volume, accounting for 16% of deals. Despite lower volumes, multi-region deals garnered the highest total capital, while the ‘Big Four’ markets Nigeria, Egypt, Kenya, and South Africa continued to dominate, collectively accounting for 55% of total deal volume and 64% of capital deployed.

Despite a modest dip in total capital, the financial technology sector remains the star performer among African VC firms. In 2024, FinTech and Digital Banks led the market, accounting for 116 deals (34% of all tech-enabled rounds) and attracting US$1.4 billion in funding. This dynamic sector encompasses cryptocurrency platforms, embedded finance, and mobile wallets specifically designed for Africa’s largely unbanked population. Its continued dominance reflects both local demand and global trends, as digital banking solutions reshape access to financial services worldwide.

In 2024, African digital banks not only demonstrated strong regional appeal but also established a strong presence on the global stage. Tyme Bank’s US$250 million Series D ranked as the third-largest digital banking investment worldwide, while Moniepoint’s US$110 million Series C was the sixth-largest. An ongoing focus on Financials drove this momentum: 44% of deals originated in the sector, capturing half of the region’s total capital, trailed by the Information Technology (14%) and Consumer Staples (11%) sectors. The e-commerce and health care sectors witness declines in 2024, largely driven by a challenging operational environment, specifically, barriers to cost-effective growth and customer acquisition

The Nigerian Tech Startups 2024 Trend

Shifting focus to Nigeria, startups in the country secured approximately $410 million in funding in 2024, according to data from ‘Africa: The Big Deal.’ This figure remains the same as 2023, indicating a relatively stable funding environment despite broader market headwinds.

Notably, two major transactions, Moove’s $110 million raise and Moniepoint’s $110 million Series C round, accounted for over half of the total capital raised, underscoring the continued investor confidence in high-growth, later-stage Nigerian startups.

In Nigeria, the venture capital market is experiencing a shift towards funding startups that integrate sustainability and social impact into their business models. This shift is largely driven by a younger generation that values ethical practices and demands transparency from companies.

The following is a summary of the top venture capital deals in Nigeria in 2024.

| S/N | Startup | Sector | Amount Raised | Lead Investors |

|---|---|---|---|---|

|

1 |

Moove |

Mobility tech |

$110M |

Mubadala, The Latest Ventures, AfricInvest, Palm Drive Capital, Triatlum Advisors, and Future Africa |

|

2 |

Moniepoint |

Fin tech |

$110M |

Development Partners International (DPI), Google’s Africa Investment Fund, Verod Capital, and Lightrock. |

|

3 |

Yellow Card |

Blockchain |

$33M |

Blockchain Capital, Coinbase, Kraken, OpenSea and Worldcoin. |

|

4 |

Konexa |

Renewable Electricity |

$18M |

Climate Fund Managers (CFM) and Microsoft’s Climate Innovation Fund |

|

5 |

Tomato Jos |

Agri Business |

$12.2M |

N/A |

BRB’s Perspective: Our take on Venture Capital

At BRB Capital, we understand that the entrepreneurial journey is fraught with challenges, from securing early-stage funding to scaling a fast-growing enterprise. As a growing Nigerian investment firm with a global presence perspective, we see venture capital (VC) as a powerful instrument for fueling innovation, stimulating economic growth, and supporting visionary founders. We have financed high-potential startups and growth-stage businesses, enabling them to thrive in Nigeria’s dynamic marketplace and beyond.

BRB’s Approach to Venture Capital

A. Sector Focus

At BRB Capital, we prioritise sectors where we see the most potential for disruption and sustainable impact in Nigeria and the broader African context. These include

| SECTOR | SUBSECTOR AND FOCUS |

|---|---|

|

Technology and Innovation |

fintech, e-commerce, software-as-a-service, healthtech, edtech, regtech, insuretech, paytech |

|

Agribusiness and Food |

sustainable agriculture, food processing, logistics, sustainable land use, circular economy |

|

Energy and Infrastructure |

Renewable power solutions, energy efficiency, smart grids |

|

Consumer Goods and Services |

FMCG, retail, lifestyle brands |

B. Staged Investments

We support businesses at various stages of growth, whether you are an early-stage startup looking for seed funding or a growth-stage enterprise seeking Series A or beyond. Our staged approach allows us to partner with entrepreneurs at various stages of their journey, helping them secure the necessary capital to innovate, refine their business models, and penetrate new markets.

C. Hands-on Advisory

Funding alone is seldom enough to ensure success. Our team of industry specialists and operational experts complements funding by collaborating with portfolio companies to provide strategic guidance, market intelligence, and mentorship. We help founders navigate challenges such as product development, market entry, regulatory compliance, team building, and governance.

D. Responsible Investment

At BRB Capital, we prioritise responsible investing. We believe in supporting companies that create positive social, economic, and environmental outcomes. By adhering to robust Environmental, Social, and Governance (ESG) principles, we strive to ensure that our investments are inclusive and purpose-driven.

Conclusion?

In conclusion, Nigeria’s venture capital ecosystem remains a cornerstone of innovation and economic diversification in Africa, despite the challenges posed by currency volatility, regulatory uncertainties, and infrastructure gaps. The persistent investor interest, especially in fintech, clean energy, and B2B commerce sectors, highlights the country’s vast potential to foster scalable, impact-driven startups that address real economic and social needs. With emerging policy reforms and growing collaboration between local and international investors, the Nigerian VC market is poised for resilient growth and continued leadership in the continent’s entrepreneurial landscape.

Looking ahead, sustaining this momentum requires fostering operational efficiency, enhancing regulatory clarity, and expanding infrastructure to unlock the full potential of Nigeria’s young, tech-savvy population. Venture capital will remain a critical enabler for innovative solutions that drive job creation, financial inclusion, and sustainable development. As Nigerian startups increasingly navigate global markets and adopt pragmatic growth models, the ecosystem is well-positioned to deliver significant economic value and cement Nigeria’s status as Africa’s foremost hub for venture investment.

Financial Planning FAQs

Common questions on Financial Planning and Investing

What should a financial plan include?

A financial plan should outline your income, expenses, assets, liabilities, savings goals, and investment strategies. It also includes retirement planning, insurance coverage, estate planning, and tax considerations, ensuring all aspects of your financial life are aligned with your short and long-term goals.

Can you help me plan for retirement?

Yes. We design retirement strategies tailored to your lifestyle goals, income needs, and risk tolerance. Our approach ensures that you build sustainable wealth, maximise your retirement income streams, and safeguard your financial independence throughout your retirement years.

What is your investment philosophy?

Our investment philosophy is centred on value creation, prudent risk management, and diversification. We focus on aligning every investment decision with your unique objectives while balancing growth opportunities with capital preservation.

Will I have a dedicated advisor?

Absolutely. Each client is assigned a dedicated advisor who understands your financial situation and goals. Your advisor will work closely with you, providing personalized guidance, ongoing support, and regular updates to help you stay on track with your financial journey.